This Week in Robotic Learning #14: What is a household robot worth?

It depends on what it can do and what your time's worth

As Weave rolled out their new $8k robot earlier this week, Chris Paxton had a good post about a few interesting new cheap robots, which motivated me to try to quantify and value the types of chores that a particular home robot might be able to do.

On the other end of things, Elon Musk has stated that he’s targeting a $20-30k range for Tesla’s Optimus humanoid. He’s also projected a lot of capability onto this thing, saying it could help with laundry and house cleaning, but eventually cooking, lawn care, and even the most sensitive of things: elder care and child care. As another market point, 1x’s NEO is on the market as a sort of “general purpose” household humanoid at a $20k price point.

Why do these things cost this much? What should they cost? It’s time to put on our consultant hats and look at the Total Addressable Market (TAM) not of robotics generally, but of the specific types of tasks that household robots might be able to do.

What I found is that the constraint is quite clearly not demand–there is ample evidence that people would pay a lot for robots that even solved a few household problems. The issue is capability. The market is real–but someone needs to build a machine capable of taking it.

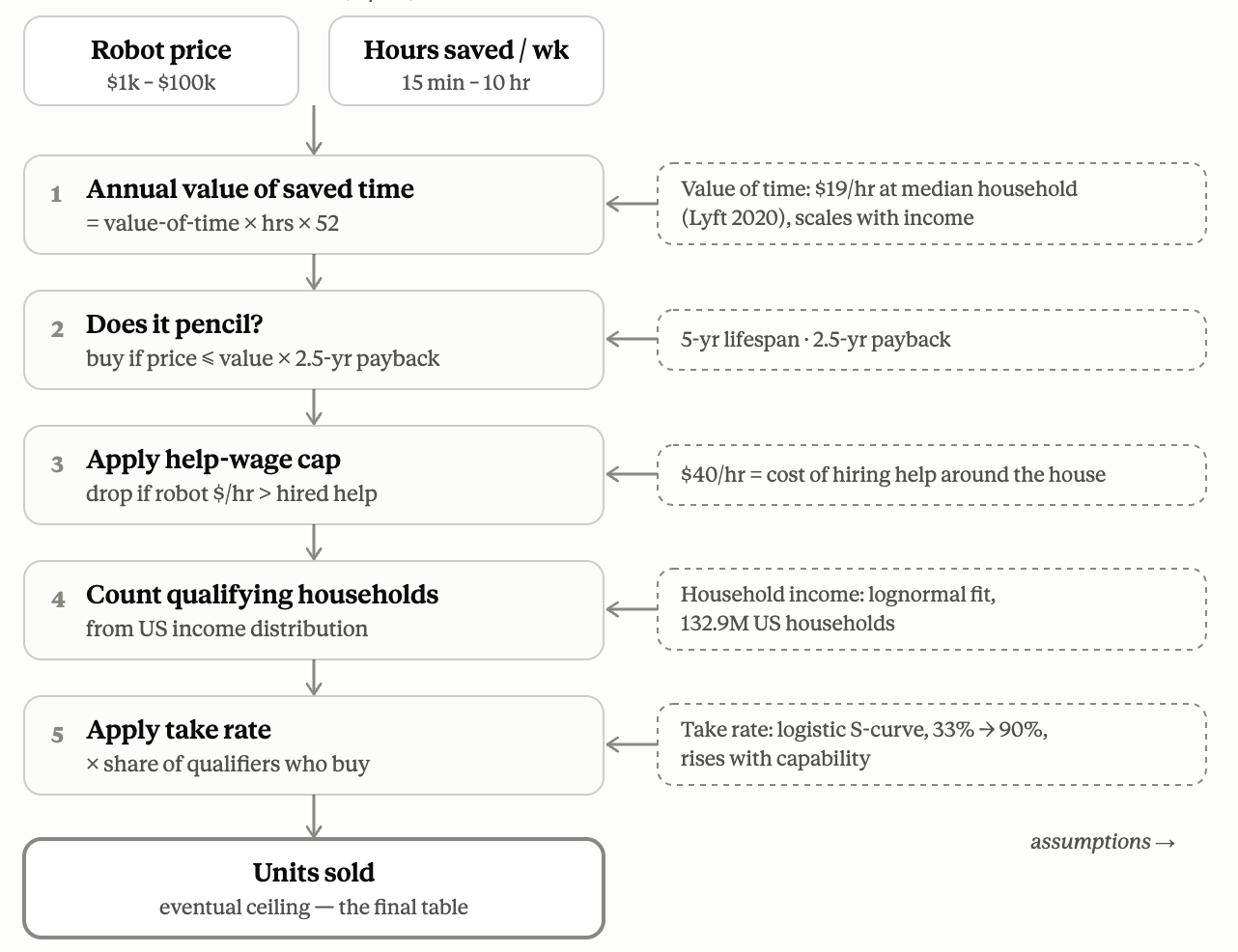

To build out a model, the best place to begin is: how long do we spend on particular tasks, and what’s the value of our time?

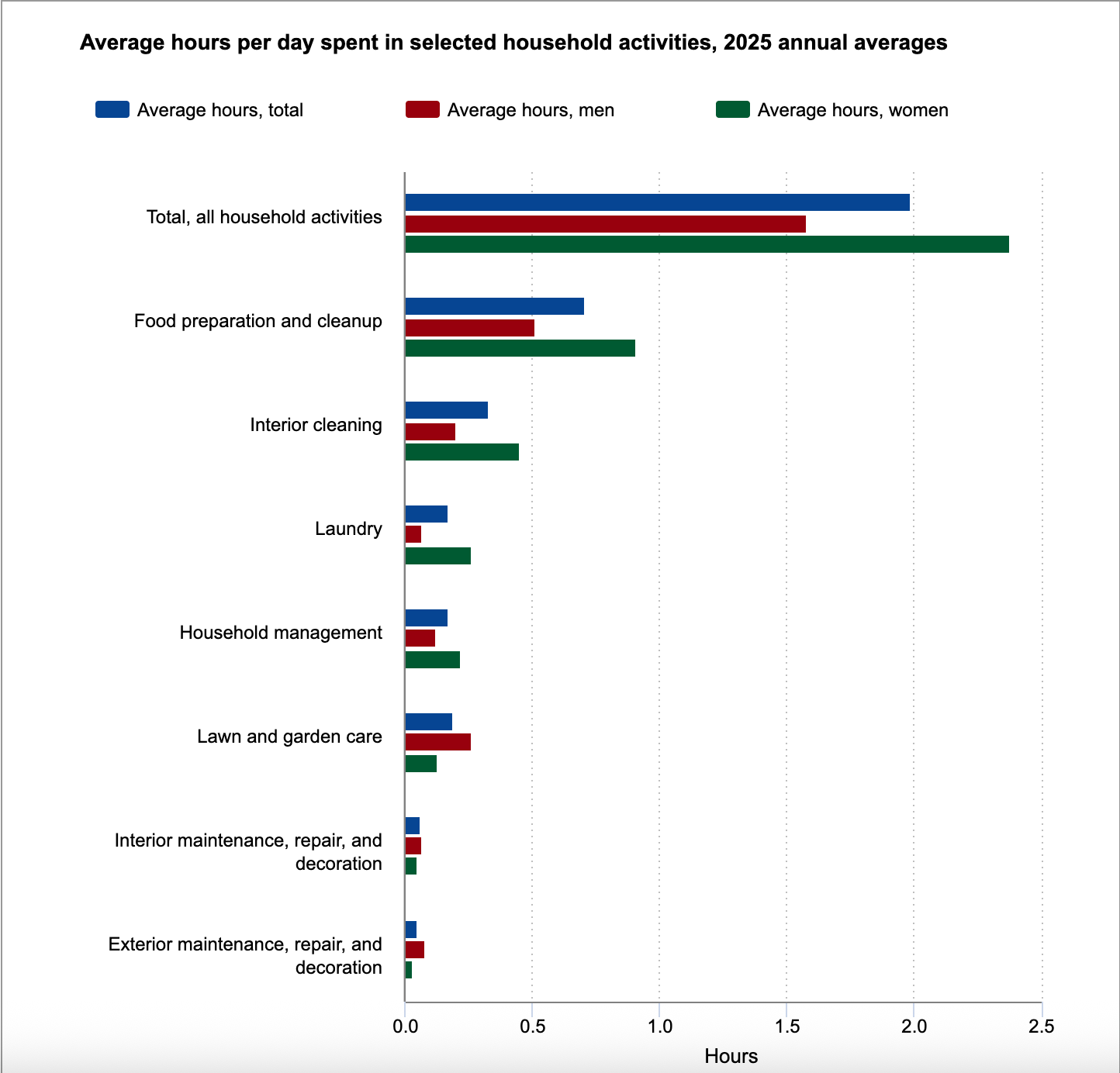

The BLS’ American Time Use Survey provides robust data on, well, American time use. Survey data isn’t perfect, but it’s literally from the Bureau of Labor Statistics, so I’m not sure what other source of labor statistics I could possibly use here.

All household activities add up to 1.99 hours per day per person. I’ll assume that this is time that could be reallocated and, if not, perhaps for a passionate chef, a robot sous chef would be more valuable as a fun toy than something that folds their laundry and saves them an hour and a half per week.

Combined with an assumption of 272 million Americans aged 15+, we have a pretty decent read on how much time is being spent in aggregate on all these tasks.

But this is too broad. An “interior cleaning” robot may only be capable of tidying, which is both incomplete in that category and bleeds over into cooking & food prep. For now, we’ll put that aside because what we need to do here is make some assumptions in the service of answering the very important high level question: how valuable is an American’s time?

Assumptions!

The model with all its math and assumptions

First and foremost, these are eventual ceilings not annual sales. There are going to be some big numbers. But it’s also worth noting that this is just looking at the United States, not globally. And the globe is big, so this understates the overall opportunity.

Gross median earnings in the United States are ~$28/hour. In a 2020 study, The Value of Time in the United States, the authors used randomized wait times and prices and found that Americans roughly value their time at $19/hour. That’s reasonably close to median net wage, and the historical literature has generally put the value of leisure time at around 50% that of gross wages, so it’s probably somewhere in the $14-19/hour range. As such, I like the figure from the Lyft study.

The next assumption is: how long can we expect this thing to last? I bought a dishwasher and it broke within three years. That was a very disappointing outcome! This is a more complex machine, so expectations should be a bit more managed; if our chore bot made it seven years, I’d dutifully say farewell. Let’s set our base case at five years.

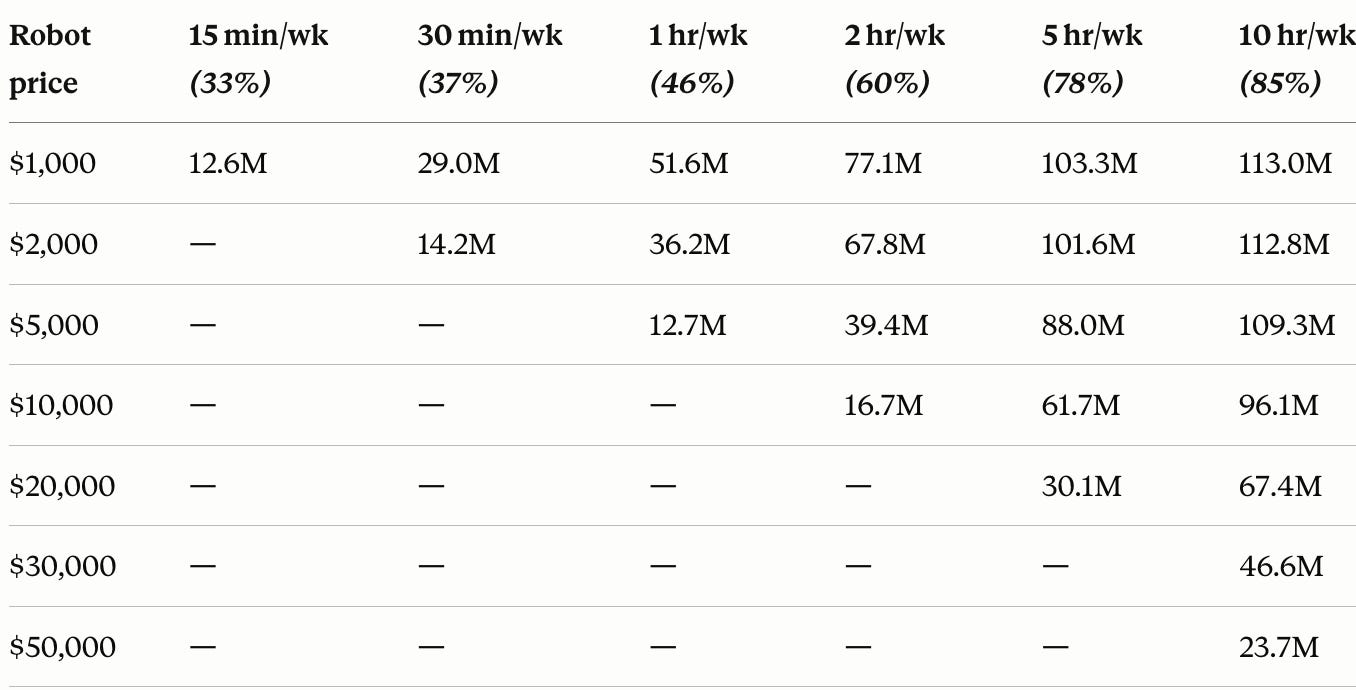

With those two assumptions in place, we have a rough sense of how much time a robot should save. If we’re pricing at $1k, we only need to save 53 hours; that’s less than one hour per month over five years. (For the sake of my sanity, we will not be doing any time value of money calculations. Deal with it.)

From here, the units shift from individuals to households, as that’s the more useful buying unit for a household appliance. The pricing tables are per household and priced off household income with a dual-earner correction.

A household’s total chore load is ~28 hr/week, so a robot saving 5 hr/week covers ~18% of total chores–not nothing, but not inconceivable.

That’s why the long-term vision of the general purpose humanoids has to be so ambitious: it’s priced below cost and is still a long way from justifying the value.

That said: you don’t need to sell a product to the median American to have it be worthwhile. Statisticians have long found that half of all people are above the median–one of those weird mathematical quirks, really, and it applies to Americans’ income too. Maybe they’ll buy some robots.

If we use the median income (~$80k) to back into the Lyft study’s $19/hour, we can fill out the rest of the table.

A key thing to understand is that these are theoretical breakeven points on pricing. The reason Apple sells a ton of (expensive) iPhones is because so many buyers value their phone way more than the breakeven price and get more surplus value than they would from a competitor phone. We’re not worried about competition right now, so there’s a little more space to roam here.

I also wanted to include the “households in band” figure to make the subtle but important point that America is big. If you can save people 1 hour per week and price at $20k, selling a million units in America seems possible. If you can save two hours per week, you’ll sell tens of millions of units. If you can save five hours per week, you might well sell a hundred million units.

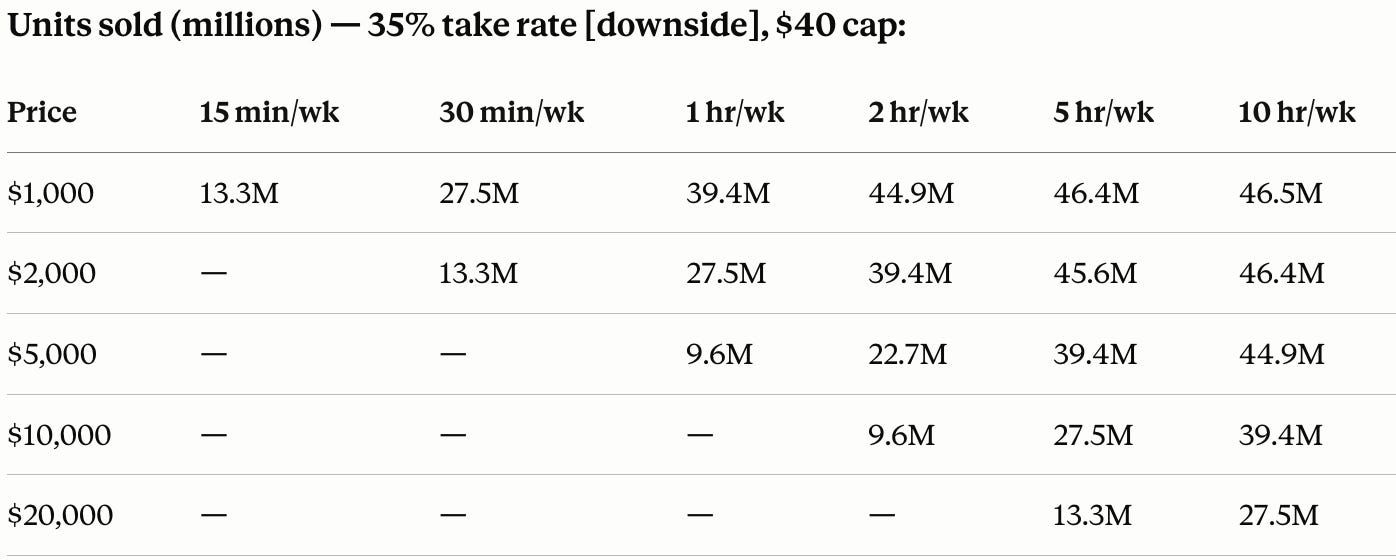

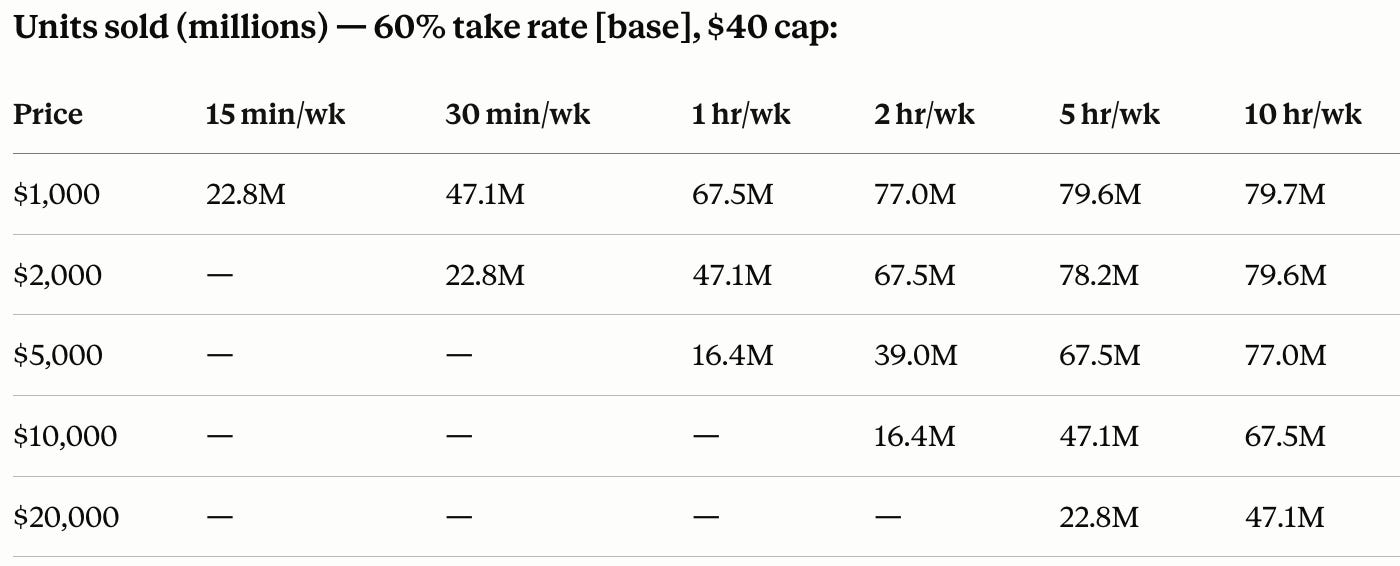

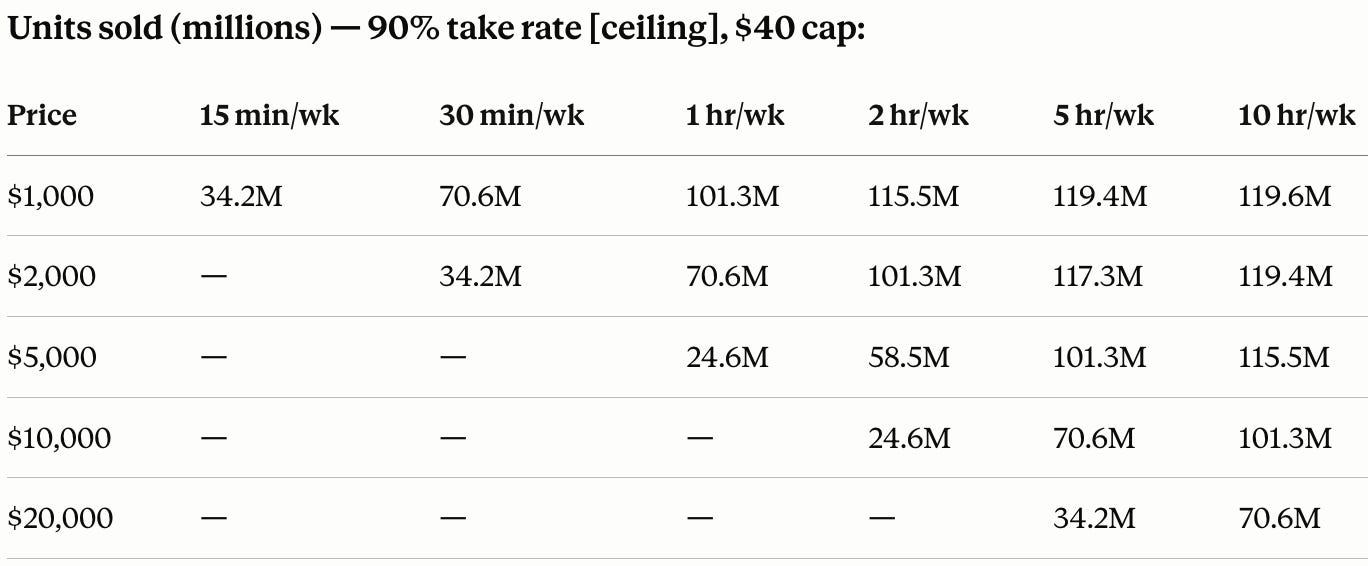

But that’s not quite right. Take a task like vacuuming: the alternative to a person with a 99th percentile income isn’t to do it themselves, it’s to hire someone else to do it. As such, let’s put a $40/hour “cap” on hiring help around the house with this sort of task. Applying that $40/hour cap makes the table look like this:

Interesting, but it seems like a lot. Would 20% of American households really pay $20k/year (that’s $100k over a 5 year life) to save an hour and a half per day?

We need to make some adjustments. So far what we’ve looked at is willingness to pay, which represents a ceiling rather than true value. We need to shift frameworks slightly, from willingness to pay to payback period, which gives us a better sense of where people actually make their buying decision. In general, the standard payback period is in the 2-3 year range.

Given that we’re already assuming a 5 year life for these products, let’s go with a 2.5 year payback period which has the mathematical convenience of just doubling the amount of value the robot needs to deliver.

The second question is the take rate. Of qualifying households, what share actually buy (net of mistrust, space, and substitutes)? Penetration of near-universal appliances is a decent proxy: microwaves ~90%, dishwashers 68%. I’ll haircut the dishwasher figure for new-category risk to a 60% base case.

If the product is more narrow and easily substituted (e.g. if it saves an hour a week, it seems plausible to be folded in to a housekeeper’s routine rather than warranting a standalone purchase), we might think the take rate is lower. Robot vacuums are in 13% of homes, so I might estimate their take rate is more like 35% of their “qualifiers” who would actually get sufficient value. If the product is both cheap, a huge time saver, and resolves the space/trust issues easily, it might approach the ceiling of microwaves.

Here are those three take rate scenarios applied, showing the price/weekly hours saved mix, with the $40/hour cap applied as a ceiling on willingness to pay.

So long as robots remain sort of experimental novelties, the downside figures are the most realistic (or possibly even over-ambitious). If we’re able to build one or two-purpose devices, the base case seems realistic. And if we’re genuinely able to replicate human capacity, the ceiling scenario is likeliest. This is the underlying insight of diffusion theory. Relative advantage–how much better the innovation is than the incumbent solution–is the strongest predictor of adoption rate and ceiling. (There are a lot of studies making this point.)

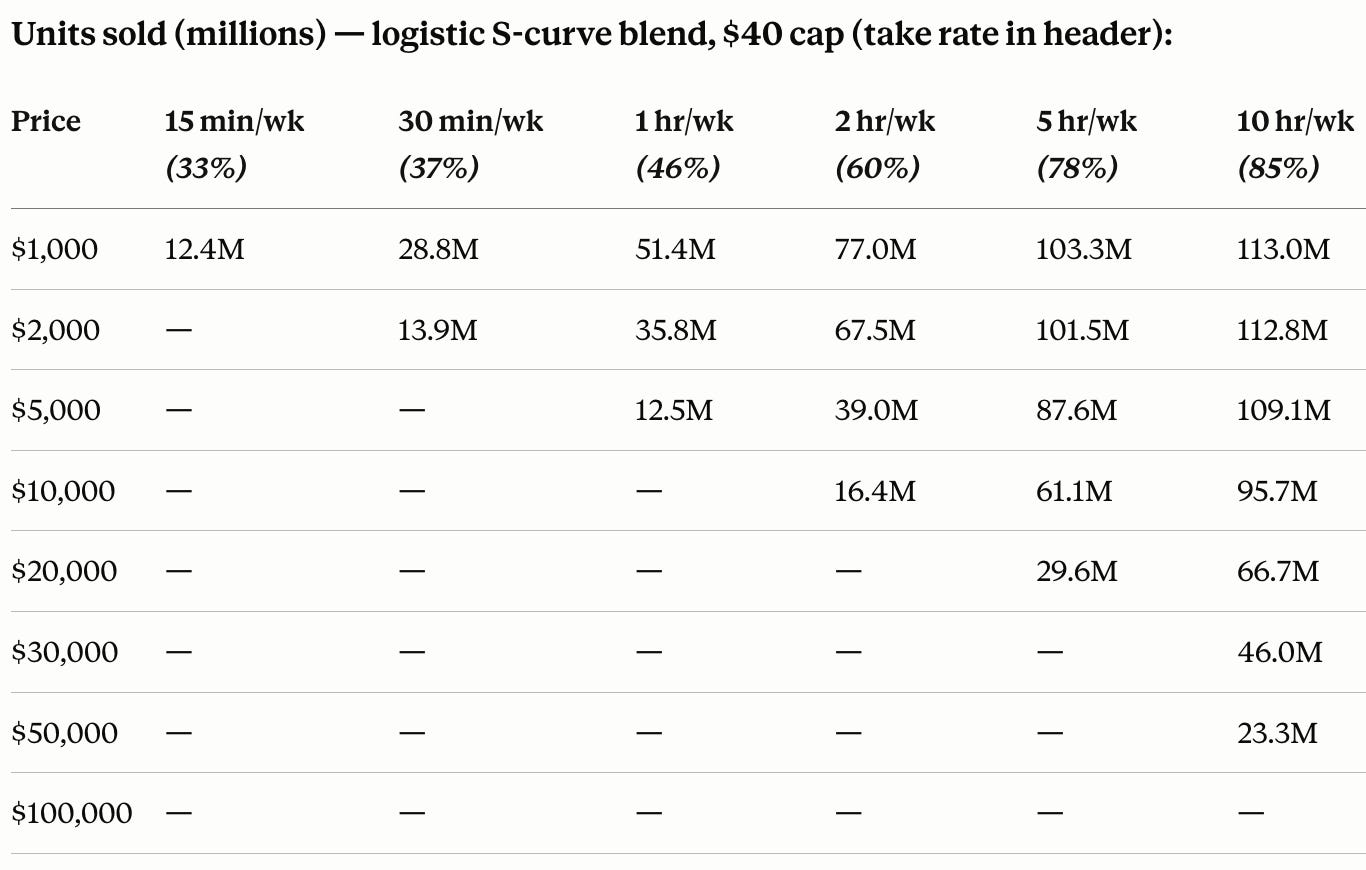

Let’s make it an S-curve because… that’s what it always actually is.

Yeah, okay, now we’re talking! I added in some higher price points just to get a better sense of what happens if we keep raising prices. My main takeaways are:

Any useful robot in the $1-2k range should be able to sell a ton of units even if it’s not that productive. So yeah: Paxton’s initial instinct on that was pretty spot-on. I think the challenge in that price range will be decoupling those tasks from general housecleaning services, but it would surely happen.

Saving 2 hours/week is where big numbers of people would be willing to make a significant investment, but the jump from 2->5 hours/week is where the huge leverage is as the take rate increases (though about ⅓ of this is driven by the take rate function).

5 hours/week is the point where they would get pretty expensive and ubiquitous.

Any robot that saves 10 hours a week will command $10k plus and sell huge numbers of units. It’s basically free money to raise the price from $1k to $10k, and doubling price to $20k means selling ⅔ as many units, so the economics work better there. The $50k price might pencil out even better, depending on what input costs are.

At a $100k price, the model shows zero units sold at any level of productivity.

What labor can be saved?

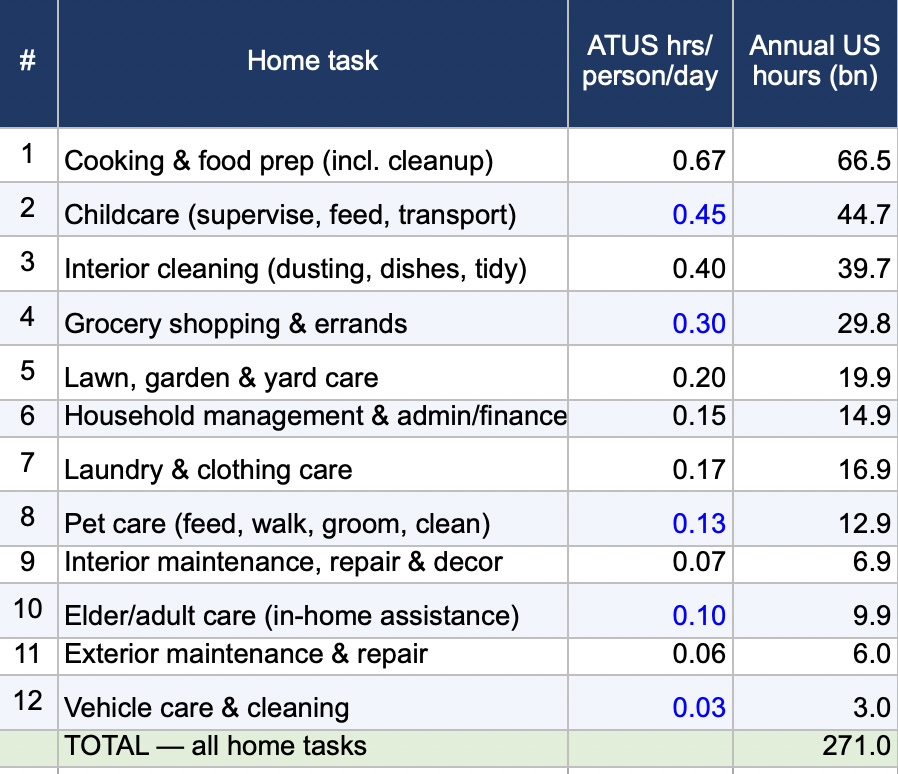

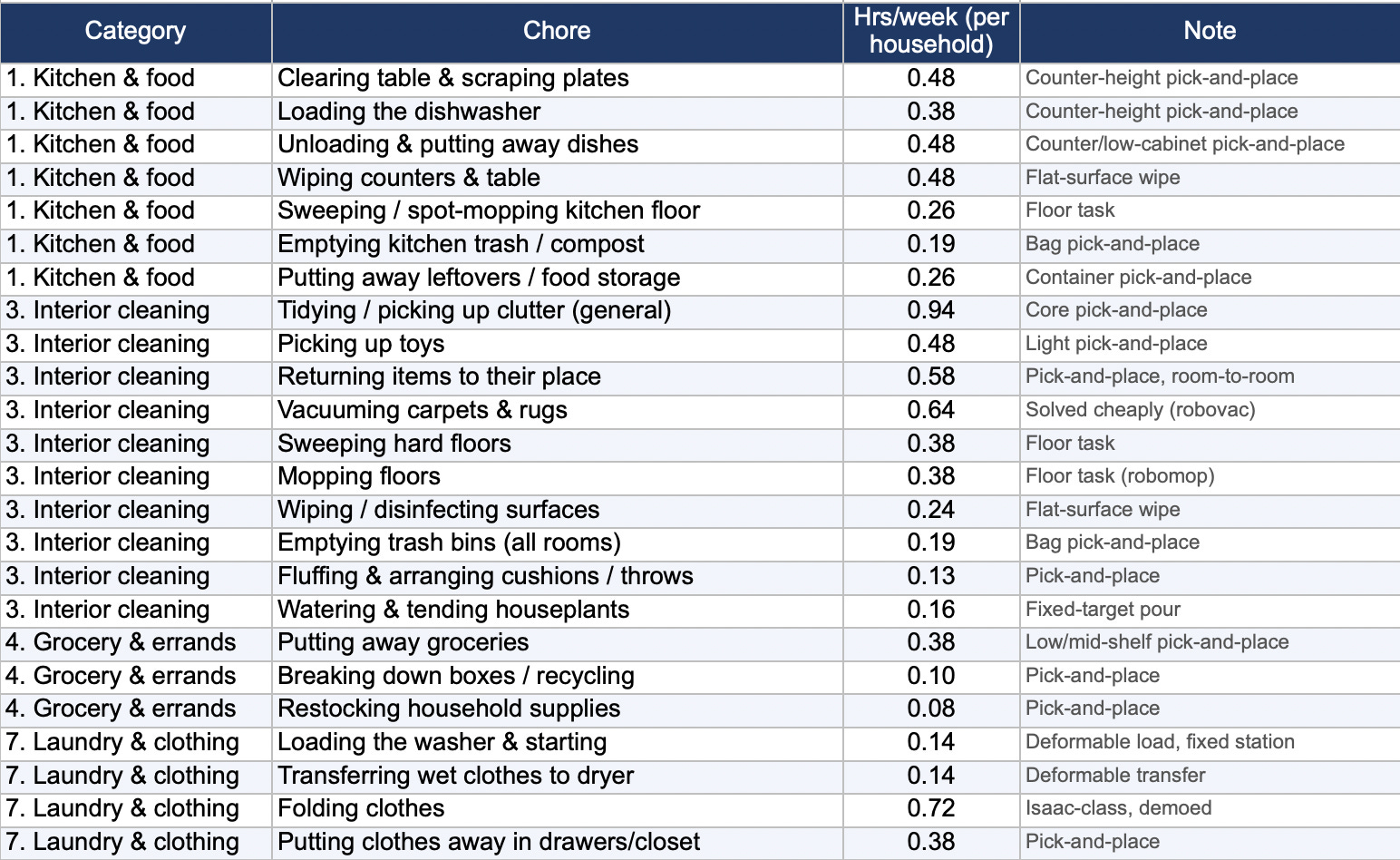

Let’s circle back to the kind of work that we’re evaluating here to assess what robots might be able to actually do. A general purpose humanoid, almost by definition can do all the tasks a human does. But what’s more interesting is where the specific points of leverage exist as we consider what a cheaper bot might need to do. Using the ATUS as our jumping off point, I identified a few tasks that seem like a potentially good fit for cheap home robots, with estimates for their time consumption.

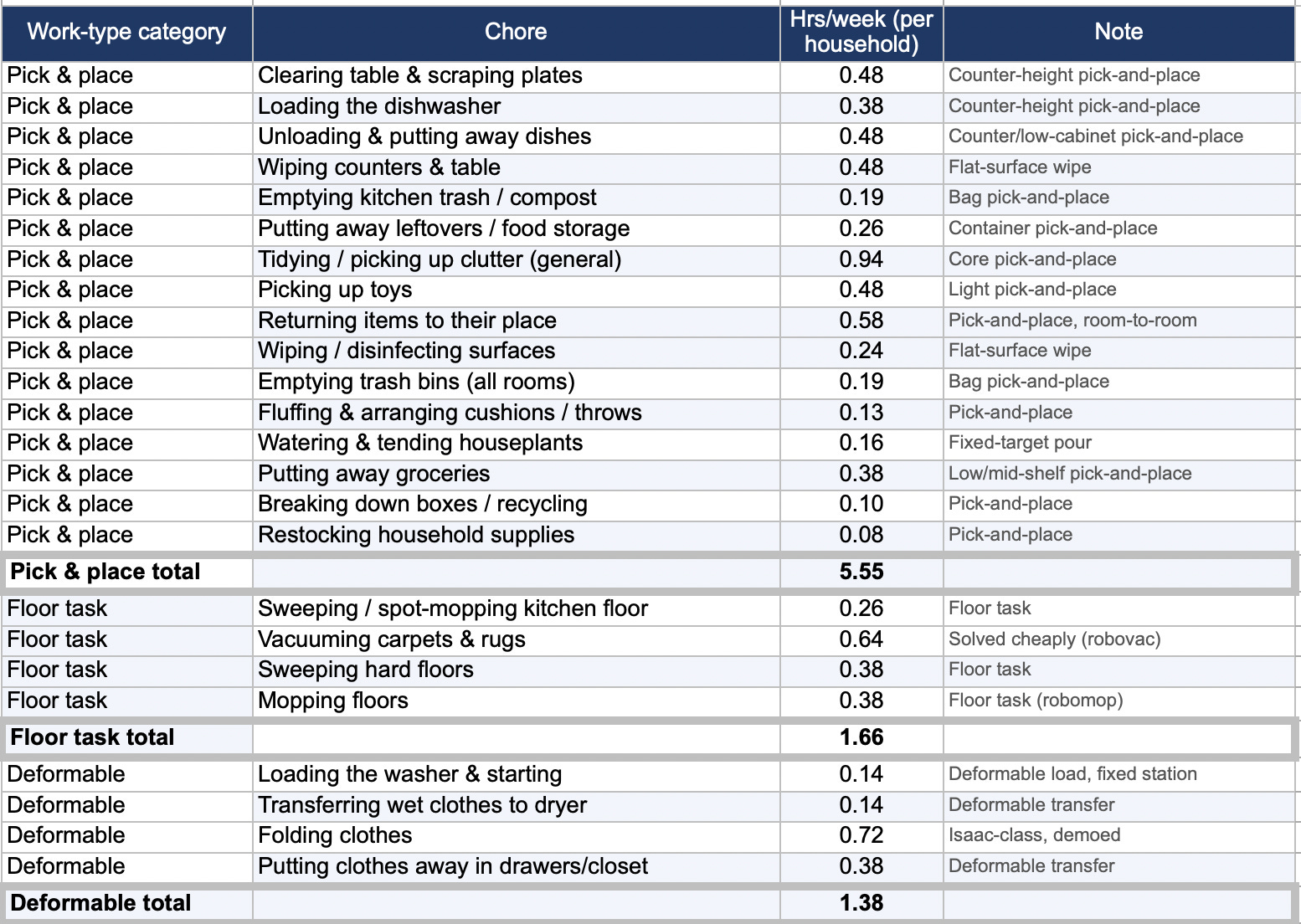

But the more useful categorization is not so much by which broad category a task falls into as what type of task it is. I think the most relevant divisions here are: floor task, pick & place and deformable objects, from least to most difficult. A specific task is categorized by whichever of the most difficult of those categorizations it involves (so “putting away laundry” is deformable objects, not pick & place). I’ll also bring back the price/units table for context.

Something like a Matic vacuum is reasonably close to capturing a bunch of the floor tasks and costs $1,245 as of today. But an hour a week isn’t that much, and they’re priced along those lines. They have obviously not sold 50 million units. Remains to be seen the extent to which that’s a “speed of penetration” vs. a “the product doesn’t really deliver that much value.” Again, I think this is in large part because vacuuming is largely bundled with housekeeping services–perhaps over time if that changes, Matic will get much more penetration.

The pick and place tasks are where the huge opportunity is, and where the needs are higher frequency, so not as easily bundled as part of, say, a weekly house cleaning.

So what?

A household pick and place bot genuinely could be worth $10k to 60 million households if it were able to capture all of that time. That’s an overestimate as the robot would need to be managed–how would it know what goes in whose room, among many other things, but even if our pick and place bot delivered two out of the total five and a half hours, a $5k price point wouldn’t be too rich for many people, and Weave’s $8k is well within the bounds of reasonable if it delivers on that promise.

Of course, for right now, the people buying even the “low-end” robots are hobbyists and enthusiasts much more so than folks whose primary concern is time savings. $8k for a product from a start-up that’s new to the market is a lot! Who knows if it works? The one thing you definitely get is a fun conversation starter. But there is a path to a huge market for any company that can make an effective pick and place bot even if it doesn’t really do much else.

The “deformable objects” add-on is difficult to judge. My initial read is: it’s kind of squeezing blood from a stone, but perhaps adding that additional capability on top of normal pick and place moves it up the take rate curve and accelerates adoption more than the surface level hour and a half of saved labor might initially appear.

What else would have to be true to get investors excited?

Cost: ~$5–8k for a pick-and-place bot would sell into tens of millions of homes. Can BOM/COGS get to a place where that price point is workable?

Timing: this is more of a TAM assessment. Will penetration happen fast enough? Robot vacuums took ~20 years to reach ~13%.

Defensibility: category TAM is not the same as any one company’s TAM. Who will actually capture the value, and how will they stave off competition? What’s the piece of the process that compounds? Intelligence? Manufacturing scale? Data/learning?

Purpose-built pick-and-place at ~$5–8k clearly presents a big, addressable base; the evidence suggests that there’s going to be bifurcation between high-end and simpler robots.

But if the realized hours are below what these tables expect, the whole thing falls apart. Investing is about being forward-looking, but at some point, someone needs to execute and actually save people all that time.

It’s clear that the market exists. All that’s left to do is meet it.

Let’s look at some robots

We have to look at the Weave robot after all that, right?

Weave is specifically focusing on the pick and place + deformable categories, and while their bot is not yet autonomous, they’re clearly taking on the very areas discussed above. Their Isaac 0 used “a blend of autonomy and teleoperation” and I assume the same is true of Isaac 1. The TAM analysis says that at an $8k price point, if they can take down pick and place & deformable categories in whole, they’ll be able to capture a huge chunk of the American market, so that’s neat! Pretty impressive stuff from a very small team.

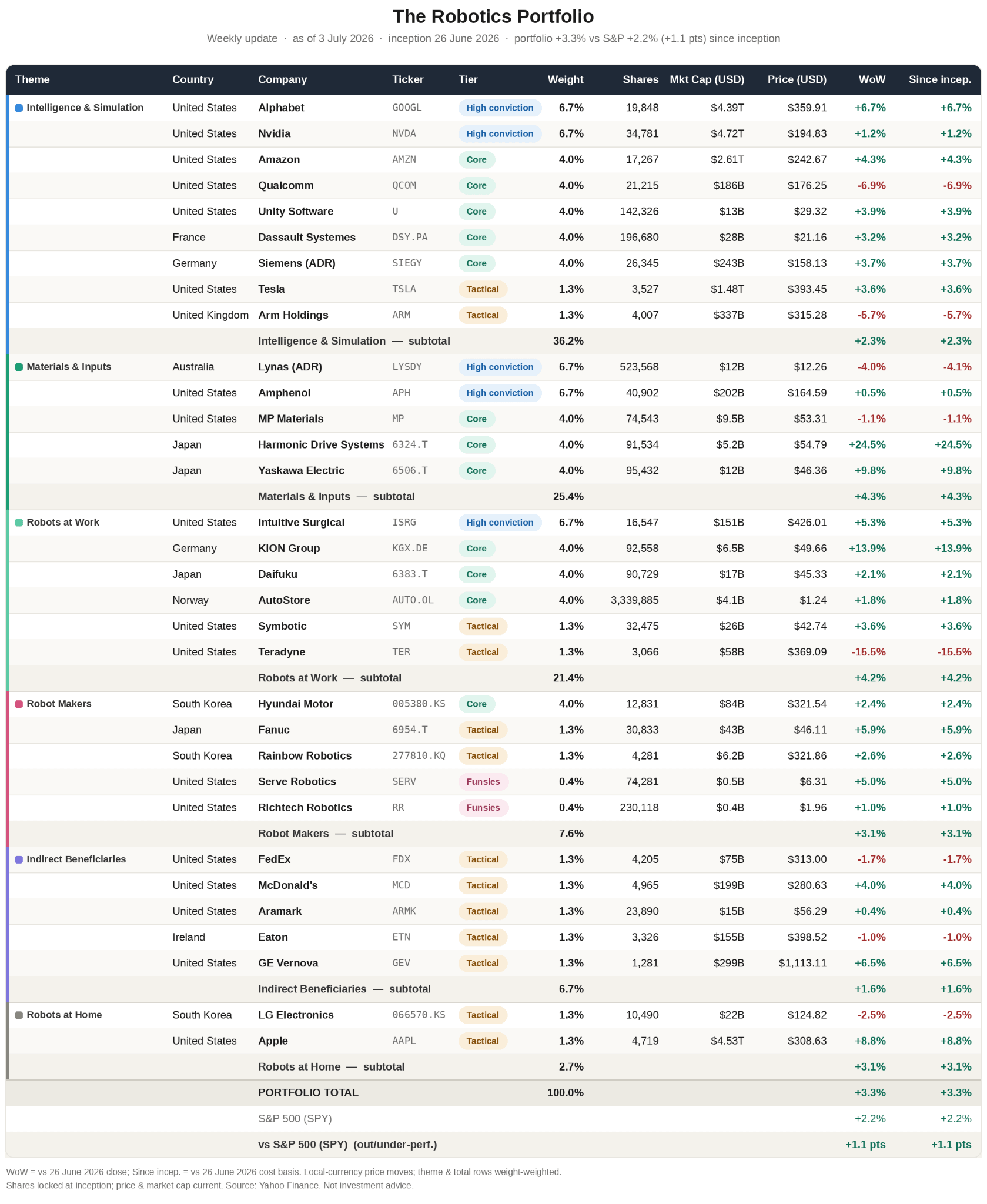

Robotics Portfolio update

A new segment in which we see how the portfolio we launched last week is performing. On the one hand, one week is not nearly long enough to see how a long-term investment thesis is playing out. On the other hand: we’re rich, baby! Overall it’s up 3.3% WoW. If we’re able to keep that up, we’ll all be retired within a year or two. Not only that, we thumped our benchmark, SPY, which was only up 2.2%. The big winner was Harmonic Drive Systems (25%) as Japan named physical AI a flagship national initiative. Teradyne (-15.5%) and Qualcomm (-6.9%) were fallers as part of a semiconductor sell-off.